The U.S. Is the Global Hotspot for Cleaning Robot Fleets

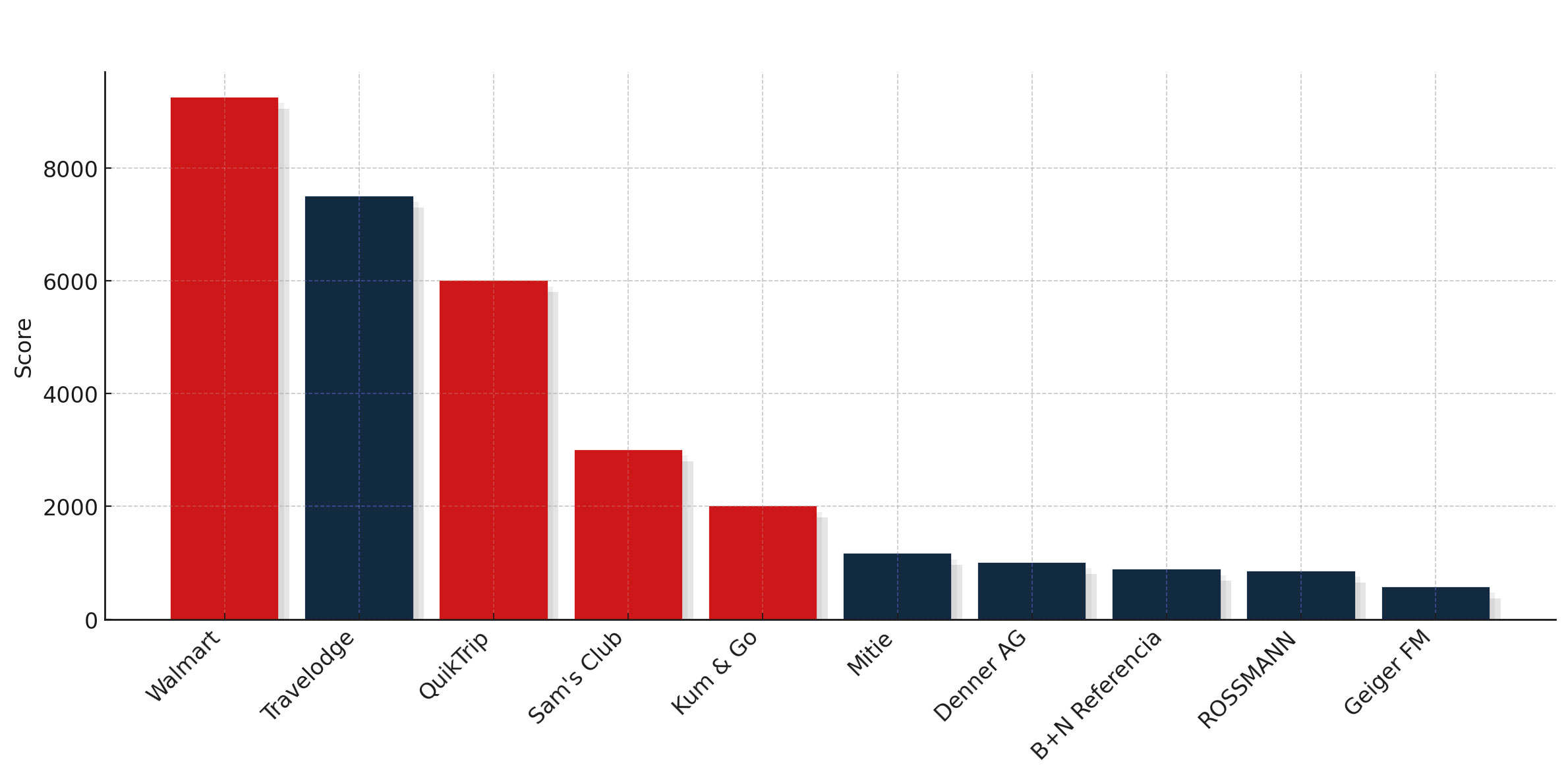

Chart 1: Top 10 Cleaning Robot Fleets 2025 by Radar Score

Grocery, Warehouse, Convenience

What makes the U.S. stand out is not simply “retail” as a single category, but the coexistence of very different store formats. Walmart and Schnucks represent the grocery chains, operating vast floor areas with predictable layouts that reward high utilization. Sam‘s Club exemplifies the warehouse club model with extreme standardization, wide aisles and large-scale throughput. Convenience chains such as QuikTrip, Kum & Go, RaceTrac or J&H Family Stores show that even smaller formats can scale fast if their layouts are standardized and their corporate structures allow centralized decision-making. Each of these models produces its own robotics pattern, but all push the U.S. further ahead of other regions.

Investment Style and ROI

The way American operators invest reinforces this dynamic. Rollouts tend to be blunt and national: once a pilot works, hundreds of machines follow. Return on investment is straightforward, because robots often replace outsourced cleaning services and the savings are easy to measure. Financing models, whether capital expenditure, leasing or OPEX contracts, are widely available, and the balance sheets of major U.S. chains support rapid, eight-figure commitments. In Europe the picture is more fragmented, with decisions often made store by store; in the U.S., scale is built into the corporate structure.

hypermarkets offer robots wide aisles and plenty of space.

OEM Concentration Under Pressure

The American Top-10 has long been shaped by Tennant hardware combined with Brain Corp autonomy. That partnership provided a reliable path to scale and gave the U.S. its uniform fleet backbone. The arrival of Pudu at QuikTrip breaks this pattern. It shows that American retailers are open to alternatives and that the OEM landscape may shift quickly once a new supplier proves

itself in one of the large national chains. The question is no longer whether Tennant–Brain Corp can scale, but whether they can defend their dominance as others enter.

Service and Integration

Distribution and service remain open questions. Traditional providers such as Imperial Dade or BradyPLUS dominate cleaning chemicals and equipment, but it is still unclear whether they can manage fleets of robots with the same efficiency. New models are emerging, among them RobotLAB with a franchise-style, robots-only service system. The U.S. may thus decide not only who supplies the machines, but also what kind of partner network supports them. Classical distributors and specialized newcomers may compete side by side in the years ahead.

A Fleet-Ready Ecosystem?

One explanation for the American lead is what could be called a fleet-ready ecosystem. Service networks are dense, there is a willingness to adjust infrastructure — alarms, restricted access,

charging logistics — and automation enjoys broad cultural acceptance. This remains more hypothesis than data point, but it helps explain why U.S. fleets are scaled faster and run larger than their European or Asian counterparts.

Beyond Retail

The ranking also shows that the U.S. presence is wide as well as tall. Contractors such as Aramark operate large fleets that rival retailers in size. Healthcare appears as an outlier, as it supplies the only significant American operator relying on microbots rather than large scrubbers. Universities and school systems, from Denver Public Schools to Penn State, are experimenting with mid-sized fleets. Pittsburgh International

Airport demonstrates that transportation hubs are joining in, while smaller travel and gas station chains extend the convenience model beyond QuikTrip and Kum & Go. The breadth of these cases underlines that the U.S. is not only strong at the top but across multiple sectors.

Outlook

The signal from 2025 is unmistakable. If every year another American chain enters the Top-10 with hundreds of robots, then the U.S. will soon constitute a market of its own for large fleets. Convenience chains are especially well positioned to accelerate, but contractors and public institutions are also beginning to scale. The dominance of Tennant and Brain Corp is no longer guaranteed, and the rise of Pudu as a credible alternative makes the contest sharper. For now,

the U.S. establishes itself as the global hotspot of cleaning robot fleets — and the race for how this dominance will be organized has only just begun.

This article is part of the results of The Biggest Fleet 2025. Click here for all results